The Coming Infrastructure Layer of Sustainability: How Corporate Sustainability Is Becoming a Data Architecture Problem

Mar 3, 2026

Corporate sustainability is undergoing a profound transformation. For much of the past two decades, sustainability has largely been understood as a matter of corporate commitments, reporting practices, and stakeholder communication. Companies have published sustainability reports, announced carbon neutrality targets, and increasingly framed environmental and social performance within the language of ESG. Yet beneath these visible developments, a deeper structural shift has been unfolding. Sustainability is gradually moving beyond the realm of narrative and disclosure, becoming instead a challenge rooted in corporate data systems, operational infrastructures, and the architecture of information that supports decision-making within modern organizations.

🎧 Listen to the AI-powered podcast version of this article here:

https://open.spotify.com/episode/7bBrU2idi9P3oOHn05uhIn?si=5l6_V1AuSJuZZTi6qvMilA

1. Introduction — Sustainability’s Quiet Structural Shift

The transformation that has taken place in the field of corporate sustainability over the past two decades is often misunderstood. In public discourse, sustainability discussions are usually framed around targets, strategies, and corporate commitments. Companies announce carbon-neutrality timelines, launch programs aimed at reducing environmental impacts, and publish sustainability reports addressed to their stakeholders. Yet the most significant structural change in sustainability has not occurred within these targets or strategies themselves, but within the information infrastructure that makes these strategies possible. Sustainability is gradually ceasing to be a communication or reporting activity and is increasingly becoming a problem of data architecture generated and managed within corporate systems.

In the early years of corporate sustainability, the field largely developed as a narrative-based reporting practice. The first sustainability reports that emerged in the late 1990s consisted of extensive texts describing companies’ environmental impacts and social responsibility initiatives. The main purpose of these reports was to provide transparency regarding the environmental and societal effects of corporate activities. However, many of these reports were heavily text-based, and the datasets used were often limited. Companies described their energy efficiency initiatives, waste reduction projects, or social responsibility programs in sustainability reports, yet the measurement methodologies and data sources underlying these activities were often not documented in a transparent manner.

One of the most influential institutions in the development of sustainability reporting during this period was the Global Reporting Initiative (GRI). With the publication of its first sustainability reporting framework in 2000, GRI provided companies with guidance on how to report environmental and social performance. The GRI standards significantly expanded the adoption of sustainability reporting, and many companies began publishing sustainability reports using this framework as a reference. Nevertheless, the approach largely relied on voluntary disclosure, and companies retained considerable discretion over which data they chose to disclose.

For this reason, the academic literature examining the early period of sustainability reporting highlights an important limitation. A study conducted by Harvard Business School noted that data standardization in early sustainability reporting was limited and that companies reported sustainability performance using different methodologies:

“Early sustainability reporting practices were largely narrative-driven and often lacked standardized metrics that would allow meaningful comparison across firms.”

— Ioannou & Serafeim, The Consequences of Mandatory Corporate Sustainability Reporting, Harvard Business School

The period between 2000 and 2015 witnessed a rapid expansion in the number of sustainability reports published worldwide. During this time, the concept of ESG (Environmental, Social, Governance) gained increasing traction in financial markets, and investors began paying closer attention to companies’ sustainability performance. Many large corporations started publishing sustainability or ESG reports alongside their annual financial reports, and sustainability teams gradually became part of the corporate organizational structure.

However, a substantial portion of sustainability reporting during this period still reflected a communication-oriented approach. Reports often consisted of long narratives, success stories, and corporate commitments. The metrics used could vary significantly across companies, and the comparability of sustainability performance remained limited. This situation made it difficult for investors and financial actors to systematically incorporate sustainability data into their decision-making processes.

Developments over the past decade have begun to change this paradigm. The potential impact of climate change risks on the financial system has increasingly become a topic of discussion, and financial institutions have started integrating sustainability data into risk analysis frameworks. One of the most significant examples of this shift is the Task Force on Climate-related Financial Disclosures (TCFD) established by the Financial Stability Board (FSB). TCFD developed a framework recommending that companies integrate climate-related risks into their financial reporting.

The TCFD framework represents a new way of thinking about sustainability. Sustainability data is no longer used solely to demonstrate environmental performance but also to analyze financial risks and opportunities. The Financial Stability Board describes this shift as follows:

“Climate-related risks are a source of financial risk and therefore fall within the mandates of central banks and financial supervisors.”

— Financial Stability Board, TCFD Final Report

These developments signal the beginning of a broader structural transformation in the sustainability field. Sustainability is increasingly moving beyond a matter of reporting or corporate communication and becoming an integral component of corporate data infrastructure. Companies can no longer simply describe their sustainability performance; they must also demonstrate the origin of the data that generates that performance, the methodologies used to calculate it, and the processes through which it is verified.

The IFRS Foundation articulates this transformation clearly:

“Investors increasingly require high-quality, transparent, reliable and comparable reporting by companies on climate and other environmental, social and governance matters.”

— IFRS Foundation, Establishing the International Sustainability Standards Board

This shift raises a fundamental question for the sustainability field. If sustainability data has become critical information influencing investment decisions, financial risk assessments, and regulatory compliance processes, then the way this data is produced and managed becomes equally important.

Consequently, the central question in sustainability is no longer simply:

How do companies report their sustainability performance?

The more fundamental question is increasingly becoming:

How is sustainability data produced, verified, and governed within corporate systems?

The primary objective of this article is to examine precisely this transformation. Why is corporate sustainability increasingly becoming a data infrastructure problem? And how is this shift reshaping the way companies manage sustainability?

2. The Narrative Era of Corporate Sustainability

The early development of corporate sustainability was largely shaped by voluntary reporting initiatives and corporate communication strategies. Beginning in the late 1990s, companies started to demonstrate greater transparency regarding the environmental and social impacts of their activities, and sustainability reports gradually became a new component of corporate reporting practices. A significant portion of the reports published during this period consisted of extensive texts describing companies’ environmental performance, social responsibility initiatives, and governance principles. The primary objective of sustainability reporting was to communicate a company’s approach to environmental and social responsibility to its stakeholders and to enhance corporate transparency.

One of the most important institutional initiatives of this period was the Global Reporting Initiative (GRI). Established in 1997, GRI aimed to create a globally applicable framework for sustainability reporting. With the publication of its first reporting guidelines in 2000, the initiative provided companies with guidance on how to disclose their environmental, social, and governance performance. GRI standards quickly became one of the most widely adopted reference frameworks in sustainability reporting, and many companies began structuring their sustainability reports according to these standards.

One of the most significant contributions of GRI to sustainability reporting was its encouragement of companies to report sustainability performance using defined indicators. Reporting categories were introduced for issues such as energy consumption, water use, waste generation, labor rights, and social impacts, and companies were encouraged to disclose information within these areas. However, the framework was largely based on voluntary participation, meaning that companies retained considerable discretion over which data they disclosed and which indicators they emphasized.

For this reason, the academic literature on early sustainability reporting highlights an important limitation: many sustainability reports relied more on corporate narrative than on standardized data. While companies often described environmental initiatives or social responsibility programs in detail, the underlying datasets and methodological approaches were frequently limited or insufficiently documented. A study conducted by Harvard Business School summarizes this characteristic as follows:

“Early corporate sustainability reports often emphasized narrative descriptions of environmental and social initiatives rather than standardized and comparable performance metrics.”

— Ioannou & Serafeim, Corporate Sustainability Reporting: A Review of the Literature

Several factors contributed to this narrative-oriented approach. First, during the early period of sustainability reporting, these reports were largely prepared by corporate communications departments. Sustainability teams were often positioned within corporate communications or corporate social responsibility units. As a result, the language of sustainability reporting frequently revolved around strategic narratives, success stories, and expressions of corporate values.

Second, during the early stages of sustainability reporting, the methodologies used to measure sustainability performance were still relatively underdeveloped. Many companies lacked the data infrastructure necessary to systematically measure environmental performance. Data related to energy consumption, operational outputs, or supply chain impacts were often stored across different operational systems and were manually consolidated when sustainability reports were prepared. This process limited both the consistency and comparability of sustainability data.

Another important function of sustainability reporting during this period was corporate reputation management. Companies used sustainability reports not only as instruments of disclosure but also as tools to strengthen relationships with stakeholders. Environmental responsibility, social contribution, and ethical governance were increasingly perceived as elements that could enhance corporate brand value and reputation. Consequently, sustainability reports frequently served as strategic communication tools that emphasized corporate commitments and values.

This narrative-oriented approach became even more pronounced with the growing prominence of the ESG (Environmental, Social, Governance) concept in financial markets. Beginning in the mid-2000s, ESG factors were increasingly incorporated into investment analysis, and investors started paying closer attention to companies’ environmental and social performance. One of the major milestones in this process was the Principles for Responsible Investment (PRI) initiative launched by the United Nations. PRI provided a global framework encouraging investors to integrate environmental, social, and governance considerations into investment decision-making.

Despite the increasing prominence of ESG, sustainability reporting during this period remained largely narrative-driven. Companies continued to rely heavily on extended textual explanations and strategic narratives in sustainability reports, while data standardization and methodological transparency remained limited. This made it difficult for investors to systematically incorporate sustainability data into financial analysis and decision-making processes.

As a result, the first phase of corporate sustainability can be characterized as a narrative-driven reporting era. This approach played an important role in raising awareness about sustainability issues and improving transparency regarding companies’ environmental and social impacts. However, it also contained significant limitations in terms of the comparability, verifiability, and analytical usability of sustainability data.

For this reason, subsequent developments in the sustainability field increasingly began to focus on a fundamental question: should sustainability reports merely represent corporate narratives, or should they generate reliable datasets that reflect the operational reality of companies?

This question ultimately marked the beginning of a new phase in the evolution of corporate sustainability.

3. Why Sustainability Became Economically Material

One of the most significant transformations in the field of corporate sustainability is the growing economic and financial importance of sustainability issues. In the early stages of sustainability, environmental and social performance were largely framed in terms of ethical responsibility, corporate citizenship, or reputation management. Over the past decade, however, the increasing linkage between sustainability issues and financial performance and risk management has fundamentally altered the economic meaning of sustainability. Sustainability is no longer viewed solely as an environmental or social concern, but also as a factor that can affect the stability of the financial system and the long-term value of firms.

One of the key drivers behind this transformation is the increasing recognition of the potential economic impacts of climate change. Climate change is not only an environmental challenge; it is also a source of risk that can directly affect production infrastructure, energy systems, agriculture, insurance markets, and financial markets. As a result, central banks, financial regulators, and investment institutions have begun to evaluate climate-related risks from the perspective of financial system stability. One of the most prominent institutional examples of this shift is the Task Force on Climate-related Financial Disclosures (TCFD) established by the Financial Stability Board (FSB).

The core premise of the TCFD framework is straightforward: climate-related risks are financial risks, and therefore they should be analyzed using the analytical tools of the financial system. The TCFD report expresses this principle as follows:

“Climate-related risks are a source of financial risk and therefore fall within the mandates of central banks and financial supervisors.”

— Financial Stability Board, TCFD Final Report

This perspective introduced a new framework for understanding how sustainability issues should be evaluated within the financial system. According to TCFD, climate-related risks can broadly be categorized into two main groups: physical risks and transition risks.

Physical risks refer to risks arising from the direct physical impacts of climate change. Rising temperatures, extreme weather events, droughts, and floods can directly affect production facilities, infrastructure, and supply chains. For example, extreme heat can strain energy infrastructure, while prolonged droughts can significantly reduce agricultural output. Such developments can have substantial economic consequences across multiple sectors.

Transition risks, on the other hand, arise from the economic transition toward a low-carbon economy. Carbon pricing mechanisms, new regulatory frameworks, technological transformation, and shifts in consumer preferences can significantly alter the economic position of certain industries. For instance, energy production models based on fossil fuels may become less economically competitive due to carbon pricing policies or regulatory changes.

The incorporation of these risks into financial analysis has dramatically increased the importance of sustainability data for investors. Investors are no longer interested solely in companies’ financial performance; they increasingly seek to evaluate how resilient firms are to climate-related risks. The IFRS Foundation describes this need as follows:

“Investors need consistent, comparable and decision-useful information about companies’ sustainability-related risks and opportunities.”

— IFRS Foundation, ISSB General Requirements for Disclosure of Sustainability-related Financial Information

As a consequence, ESG data has begun to play an increasingly important role in financial modeling processes. Investment funds, insurance companies, and portfolio managers are incorporating sustainability data into risk analysis, portfolio optimization strategies, and long-term valuation models. For example, the carbon intensity of an energy company or the supply chain emissions of a manufacturing firm may become important inputs when investors evaluate a company’s future cost structure and strategic resilience.

Another reason for the growing economic relevance of ESG data is the potential impact of sustainability performance on a firm’s cost of capital. An increasing number of studies in financial literature suggest that there may be a relationship between ESG performance and capital costs. Firms with stronger sustainability performance may be perceived by investors as lower-risk investments and may therefore gain access to capital at lower costs.

A comprehensive literature review conducted by Oxford University summarizes this relationship as follows:

“The majority of studies find that companies with strong sustainability performance tend to experience lower costs of capital and better operational performance.”

— Clark, Feiner & Viehs (2015), From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance

These developments have significantly strengthened the role of sustainability data within the financial system. Sustainability performance is no longer evaluated solely through the lens of ethics or corporate responsibility; it is increasingly analyzed through the frameworks of financial performance, risk management, and long-term value creation.

This transformation is also reshaping the nature of sustainability reporting itself. If sustainability data is to be used in investment decisions, risk analysis, and portfolio management processes, then the reliability and comparability of this data become critical. Investors require standardized datasets that allow them to compare the sustainability performance of different companies and integrate this information into financial models.

For this reason, sustainability reporting is increasingly evolving toward a logic similar to that of financial reporting. Data quality, methodological transparency, and comparability are becoming core characteristics of sustainability information. The IFRS Foundation emphasizes this need in the following terms:

“High-quality sustainability information is essential for efficient capital allocation in global financial markets.”

— IFRS Foundation, ISSB Strategic Direction

In conclusion, the growing economic materiality of sustainability issues represents the beginning of a new phase in the evolution of corporate sustainability. Sustainability is no longer merely a matter of environmental performance or corporate responsibility; it has become an integral component of financial risk management, investment decision-making, and capital allocation processes.

This development also introduces new requirements regarding the production, management, and verification of sustainability data. If sustainability data is to inform financial decision-making, then the reliability, transparency, and methodological rigor of that data must be equally robust.

4. The Rise of Mandatory Sustainability Reporting

One of the most significant structural transformations in corporate sustainability is the gradual shift of sustainability reporting from a voluntary corporate practice to a regulatory requirement. In the early stages of sustainability reporting, companies typically disclosed their environmental and social performance within voluntary frameworks. Standards such as the Global Reporting Initiative (GRI) provided reporting guidance, but the preparation of sustainability reports or the disclosure of specific data points was rarely a legal obligation. As a result, sustainability reporting remained for many years a practice largely shaped by companies’ own preferences and priorities.

Over the past decade, however, the growing economic and financial importance of sustainability issues has led regulators to intervene more directly in this domain. As the potential impact of climate change on the financial system has become increasingly evident, regulatory authorities have begun to require companies to disclose sustainability-related information in a more systematic manner. This development has fundamentally altered the nature of sustainability reporting. Sustainability reporting is no longer viewed solely as a tool for corporate transparency; it is increasingly seen as a critical source of information for the functioning of financial markets.

One of the most prominent examples of this transformation is the Corporate Sustainability Reporting Directive (CSRD) introduced by the European Union. CSRD represents one of the most comprehensive regulatory frameworks designed to transform sustainability reporting into a mandatory disclosure regime. Developed by the European Commission, the directive requires approximately 50,000 companies operating in Europe to publish sustainability reports in accordance with standardized reporting requirements. These companies must disclose not only their environmental performance but also their social impacts, governance practices, and sustainability-related risks in a systematic and structured manner.

Under CSRD, sustainability reports must be prepared in accordance with the European Sustainability Reporting Standards (ESRS). The ESRS framework defines a comprehensive disclosure architecture for sustainability reporting. These standards cover hundreds of data points across environmental, social, and governance topics and require companies to disclose this information using clearly defined methodologies. The European Commission describes the objective of this regulation as follows:

“Companies will have to report standardized information on sustainability risks and impacts, making the information more comparable and reliable.”

— European Commission, Corporate Sustainability Reporting Directive

This development has dramatically expanded the scope of sustainability reporting. Companies can no longer rely solely on reports that describe general sustainability strategies; they must now produce detailed disclosures based on specific metrics, structured data points, and standardized methodologies.

The developments in Europe are also part of a broader transformation occurring at the global level. The International Sustainability Standards Board (ISSB), established by the IFRS Foundation, aims to develop globally applicable sustainability reporting standards. The standards developed by ISSB focus particularly on the investor perspective and seek to explain how sustainability issues affect financial performance.

The IFRS Foundation describes the direction of sustainability reporting in the following terms:

“The global economy needs consistent, comparable and decision-useful sustainability information for investors.”

— IFRS Foundation, ISSB Mission Statement

The emergence of ISSB standards represents an important step toward greater global convergence in sustainability reporting. Achieving a degree of alignment between sustainability reporting frameworks developed across different jurisdictions will enable investors to more easily compare companies operating in different markets.

These developments are gradually bringing sustainability reporting closer to the architecture of financial reporting. Traditionally, financial reporting relies on a disclosure logic in which specific data points must be reported in standardized formats. This logic is increasingly being adopted in sustainability reporting as well. As a result, the boundaries between financial reporting and sustainability reporting are becoming progressively blurred.

One of the most significant consequences of this transformation is the dramatic increase in the volume of data that companies must produce. In the early years of voluntary sustainability reporting, companies typically disclosed performance using a relatively limited set of indicators. New regulatory frameworks, however, require the production of much larger datasets. Detailed data points are now defined across numerous domains, including energy consumption, carbon emissions, water usage, supply chain impacts, labor practices, and governance structures.

This shift is fundamentally changing the technical nature of sustainability reporting. Sustainability reports are no longer merely narrative documents; they are increasingly becoming technical disclosure systems containing extensive datasets. The growing number of disclosure requirements and data points has made the preparation of sustainability reports significantly more complex.

These developments raise an important question for companies. If sustainability reporting is evolving into a comprehensive disclosure regime involving hundreds of data points, the methods by which this data is produced and managed become critically important. Preparing sustainability reports is no longer simply a process handled by corporate communications departments; it has become a technical process requiring data engineering, data governance, and integration with corporate information systems.

Consequently, the regulatory transformation of sustainability reporting has done more than increase reporting obligations. It has fundamentally changed the nature of sustainability management. Companies must now develop data infrastructures capable of systematically generating sustainability information from their operational systems. This shift is driving the sustainability field toward a new phase increasingly centered on data infrastructures and information systems.

5. Sustainability as a Data Architecture Problem

One of the most critical yet often overlooked realities in the field of corporate sustainability is that sustainability performance is not a directly observed dataset. Metrics such as a company’s carbon footprint, water consumption, energy intensity, or supply chain emissions are rarely single measurements that can be directly observed. Instead, these indicators are typically derived through calculations based on operational activities. In other words, sustainability data emerges from the processing of multiple operational data sources through specific methodological frameworks. This characteristic transforms sustainability reporting from a simple communication exercise into a problem of corporate data architecture and data engineering.

The datasets used to calculate a company’s sustainability performance are typically distributed across multiple operational systems. Energy consumption may be stored in facility management systems or energy monitoring platforms. Data related to production activities often resides in manufacturing execution systems or operational management platforms. Procurement and supply chain data are commonly stored in enterprise resource planning (ERP) systems, while logistics operations, transportation flows, and product distribution data may exist in separate logistics management platforms. For sustainability reporting purposes, these heterogeneous datasets must be collected, cleaned, standardized, and transformed into a common data model before they can be used.

For this reason, sustainability performance is often the result of a basic transformation pipeline:

Consider, for example, the calculation of carbon emissions from a manufacturing facility. Carbon emissions are rarely measured directly at the facility level. Instead, operational data—such as energy consumption, fuel types used in production processes, and material inputs—is collected. These datasets are then converted into carbon emission estimates using emission factors, which translate activity data into greenhouse gas emissions.

A similar process occurs when estimating supply chain emissions. Procurement records, product categories, and supplier activity data are combined with standardized emission factors to estimate the carbon footprint of purchased goods and services. This process is commonly used in Scope 3 emissions accounting, where emissions are derived from supply chain activities rather than direct measurement.

One of the most critical components of this calculation process is the use of emission factors. Emission factors represent the amount of greenhouse gas emissions associated with a unit of activity—for example, the carbon emissions associated with consuming one megawatt-hour of electricity. However, emission factors are not fixed or universal values. They vary significantly depending on the methodology used, the geographic region, and the energy mix of the electricity system. The International Energy Agency (IEA) emphasizes this methodological variability:

“Emission factors can vary significantly depending on methodology, system boundaries and regional energy mixes.”

— International Energy Agency, Emission Factors Database

Because of these variations, the methodologies and data sources used in sustainability calculations must be carefully documented. Without methodological transparency, it becomes extremely difficult to compare sustainability performance across companies or across reporting frameworks.

Another factor that increases the technical complexity of sustainability data is its dependence on operational systems. In many companies, sustainability reports are still produced through manual data collection processes. Energy data may be requested from facility management teams, production data from operations departments, and procurement data from supply chain teams. These datasets are then manually consolidated—often in spreadsheet-based workflows—before calculation methodologies are applied to generate sustainability metrics.

This approach introduces significant risks in terms of data reliability. Manual data collection processes are vulnerable to data entry errors, inconsistencies between departments, and methodological drift over time. Regulators and financial institutions have increasingly recognized this challenge. For example, the Network for Greening the Financial System (NGFS) highlights the need for robust climate-related data frameworks, noting that standardized and reliable datasets are essential for effective climate-related financial disclosure.

As a result, the production of sustainability data is increasingly viewed as a data integration and data architecture challenge. Integrating data from multiple operational systems into a unified sustainability data model presents substantial engineering complexity. Differences in data formats, variations in data quality, and the need to manage continuous data updates are among the major technical challenges faced by organizations.

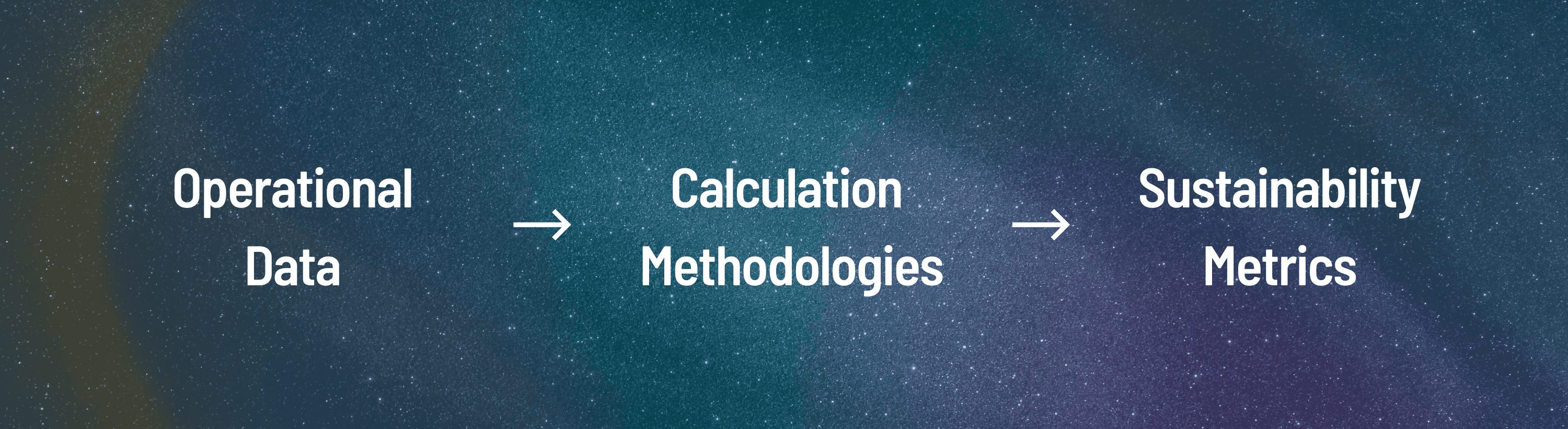

From a corporate data architecture perspective, sustainability reporting can be conceptualized as a system consisting of three primary layers.

The first layer consists of operational data sources. This layer includes datasets related to energy consumption, manufacturing operations, logistics flows, procurement activities, and supply chain interactions. These datasets represent the raw operational inputs required to calculate sustainability performance.

The second layer is the calculation layer. Within this layer, operational data is transformed into sustainability metrics through the application of calculation methodologies. Emission factors, methodological frameworks, and data transformation models operate within this layer to convert raw activity data into measurable sustainability indicators.

The third layer is the disclosure layer. This layer represents the stage where calculated sustainability metrics are transformed into reporting outputs and disclosures for stakeholders. Sustainability reports, regulatory disclosures, ESG datasets, and investor-facing sustainability information are all generated within this layer.

This architectural perspective makes clear why sustainability reporting is increasingly becoming a data architecture problem. If sustainability performance is derived from operational data, then the way in which that data is collected, processed, and governed directly determines the reliability of sustainability reporting outcomes.

Consequently, sustainability management must become increasingly integrated with corporate data infrastructures. The transformation occurring in sustainability is therefore not merely about the emergence of new reporting standards. The deeper transformation concerns how companies produce, structure, and govern sustainability data.

To measure sustainability performance reliably, companies must develop data architectures capable of collecting operational data from internal systems, managing complex calculation methodologies, and producing disclosures compatible with multiple reporting frameworks. In this sense, one of the most significant developments in the sustainability field is the gradual integration of sustainability management into the core data infrastructure of modern organizations.

6. The Data Quality Problem

One of the most critical—yet often least discussed—challenges in the field of corporate sustainability is data quality. As the scope of sustainability reporting expands and sustainability information becomes increasingly integrated into financial systems, the reliability and consistency of this data have become significantly more important. Investors, regulators, and financial institutions are increasingly using sustainability data for risk analysis, portfolio management, and long-term investment decisions. As a result, the accuracy of sustainability data is no longer merely a corporate reporting issue; it has become a matter with implications for the stability of financial markets.

However, the production of sustainability data is inherently complex. Sustainability performance is rarely a directly measured dataset; it is typically derived from operational activities through calculated estimations. This means that the quality of sustainability data depends heavily on the accuracy of underlying data sources, the consistency of the methodologies applied, and the transparency of the calculation processes used. The Financial Stability Board (FSB) highlights this challenge in the following terms:

“Inconsistent methodologies and gaps in climate-related data remain a major obstacle to the effective use of sustainability information in financial decision-making.”

— Financial Stability Board, TCFD Status Report

This data quality challenge manifests in several different dimensions. First, data gaps remain a significant issue in sustainability reporting. Many companies do not systematically collect the datasets necessary for sustainability reporting within their operational systems. Data related to energy consumption, supply chain activities, or logistics operations may be stored across different systems, and integrating these datasets for sustainability reporting often requires manual consolidation. In multinational corporations, data collection methods may differ across geographic regions, further complicating efforts to ensure data consistency.

One of the most prominent areas where data gaps occur is Scope 3 emissions. Scope 3 emissions refer to indirect emissions that occur throughout a company’s value chain and often represent the largest portion of a firm’s overall carbon footprint. However, calculating these emissions requires collecting data from external actors. Information must be obtained from suppliers, logistics providers, product use phases, and other participants across the value chain. In many cases, such data may be incomplete or based on estimates rather than direct measurement. The Greenhouse Gas Protocol describes this challenge as follows:

“Scope 3 emissions are often the largest source of emissions for companies, yet they are also the most difficult to measure due to limited data availability.”

— GHG Protocol, Corporate Value Chain (Scope 3) Standard

A second major factor affecting the reliability of sustainability data is methodological variation. Different companies may apply different methodologies when calculating sustainability metrics. For instance, system boundaries used in carbon accounting, data collection methods, or calculation assumptions may vary across organizations. As a result, two companies with similar operational activities may report significantly different carbon emission values.

One of the most visible examples of methodological variation concerns emission factors. Emission factors represent the amount of carbon emissions associated with a unit of activity and form a core component of greenhouse gas accounting. However, emission factors may be calculated differently across datasets and methodological frameworks. Differences in energy generation mixes, regional energy systems, and data sources can significantly influence emission factor values. The International Energy Agency (IEA) warns about this variability:

“Emission factors can vary significantly across datasets depending on methodology, system boundaries and geographic assumptions.”

— International Energy Agency, Tracking Clean Energy Progress

Such variability creates significant challenges for the comparability of sustainability data. Even if two companies consume the same amount of energy, the reported carbon emissions may differ depending on the emission factors applied. Consequently, the reliability of sustainability data depends not only on the datasets used but also on the transparency of the methodologies underlying the calculations.

A third major dimension of the data quality challenge concerns the reliability of supply chain data. In many industries, supply chain emissions account for the majority of total carbon footprints. However, supply chain data typically originates from actors outside the reporting company, making verification more difficult. Suppliers may have limited capacity to collect sustainability data or may rely on different reporting methodologies. This makes it challenging for companies to calculate supply chain emissions with high accuracy.

Because of these limitations, many companies estimate Scope 3 emissions using industry-average datasets or spend-based models. These approaches use average emission intensities associated with particular economic activities to estimate emissions based on procurement spending. While such methods provide practical approximations, they do not rely on actual operational data and therefore may reduce the precision of emission estimates.

Another important challenge related to the reliability of sustainability information is the inconsistency among ESG data providers. Many investors rely on ESG ratings produced by providers such as MSCI, Sustainalytics, or Refinitiv to evaluate corporate sustainability performance. However, academic research has shown that different ESG rating providers often produce significantly different evaluations for the same company. A study conducted by researchers at MIT Sloan School of Management demonstrates this divergence:

“The correlation between ESG ratings from different providers is surprisingly low, reflecting differences in methodologies, scope and measurement approaches.”

— Berg, Koelbel & Rigobon, Aggregate Confusion: The Divergence of ESG Ratings, MIT Sloan

The primary reason for these discrepancies is the use of different methodologies by ESG rating agencies. Different organizations rely on different data sources, weighting systems, and evaluation criteria. This variation raises important questions regarding how ESG data should be interpreted by investors and financial institutions.

In summary, data quality represents one of the most significant challenges in corporate sustainability. Data gaps, methodological inconsistencies, variability in emission factors, and limitations in supply chain data can all directly affect the reliability of sustainability information. As a result, new approaches aimed at improving data quality in sustainability reporting are becoming increasingly important.

These developments are also contributing to the emergence of a new discipline within the sustainability field: sustainability data governance. This approach seeks to ensure that sustainability data is systematically managed within corporate systems, that methodologies are transparently documented, and that data sources are verifiable. If sustainability information is to be used effectively in economic decision-making processes, its reliability, traceability, and comparability become essential prerequisites.

7. The Infrastructure Layer of Sustainability

One of the most significant transformations in the sustainability field is the gradual integration of sustainability management into the core data infrastructure of corporations. In the early stages of sustainability reporting, companies largely reported sustainability performance through manual processes. Data collected from different departments was consolidated in spreadsheets, calculation methodologies were applied, and the results were converted into report formats. However, as the scope of sustainability reporting expanded and regulatory frameworks introduced more detailed data requirements, it became clear that this approach was no longer sustainable. As the volume and complexity of sustainability data increased, companies began to require technical infrastructures capable of managing this data systematically.

This shift has led to the emergence of a new technological layer in the sustainability domain. This layer is increasingly described as sustainability data infrastructure. Sustainability data infrastructure refers to the corporate data systems designed to collect, process, and report sustainability-related information. These systems transform sustainability management from a process focused primarily on reporting into a data architecture integrated with operational systems.

One of the key systems driving the development of sustainability data infrastructure is the emergence of sustainability data platforms. These platforms aim to consolidate data originating from different operational systems into a unified sustainability data model. Data sources such as energy consumption records, production activities, procurement transactions, and logistics movements are integrated within these platforms. Through this integration, sustainability data becomes a natural component of the corporate data architecture and can be used across multiple reporting and analytical processes.

Another important component of sustainability data infrastructure is carbon accounting infrastructure. Carbon accounting infrastructure includes the data models and calculation methodologies required for companies to systematically calculate their carbon emissions. These systems connect operational data with emission factors and calculation algorithms to estimate greenhouse gas emissions. Within these systems, the systematic management of methodologies and emission factors is particularly important. Changes in emission factors, methodological assumptions, or data sources can significantly alter carbon accounting results, making governance and transparency essential components of the system.

A further critical element in the development of sustainability infrastructure is the emergence of ESG data pipelines. ESG data pipelines refer to the data processing workflows that collect sustainability data from multiple sources, clean and standardize that data, and transform it into analyzable datasets. These pipelines are typically designed as part of a company’s broader data engineering architecture. Automated data extraction from energy monitoring systems, integration of supply chain datasets, and automated updates of carbon calculations are typical components of ESG data pipelines.

The most comprehensive form of corporate sustainability data infrastructure can be found in enterprise sustainability systems. These systems treat sustainability management as an integrated part of corporate operations and connect sustainability data with financial data, operational data, and risk management systems. This integration transforms sustainability management from a reporting function into an information infrastructure that supports strategic decision-making.

From a data architecture perspective, sustainability data infrastructure can generally be conceptualized as consisting of three primary layers.

The first layer is the data collection layer. At this stage, sustainability-related data is gathered from operational systems. Energy consumption data, production activities, procurement records, and supply chain movements are integrated within this layer. Data quality controls and standardization processes play a critical role at this stage to ensure consistency across datasets.

The second layer is the calculation layer. Within this layer, operational data is transformed into sustainability metrics. Indicators such as carbon emissions, energy intensity, water consumption, and waste generation are calculated at this stage. The emission factors, methodologies, and data transformation models used in these calculations determine the accuracy and reliability of sustainability performance metrics.

The third layer is the disclosure layer. This layer prepares sustainability data for different reporting frameworks and stakeholder requirements. Reporting standards such as CSRD, ISSB, and TCFD require specific data points to be disclosed in structured formats. The disclosure layer ensures that sustainability data is transformed into the formats required by these reporting frameworks.

This three-layer architecture clearly illustrates why sustainability management is increasingly becoming a data infrastructure challenge. If sustainability reports now consist of complex disclosure systems covering hundreds of data points, then these data points must be produced and managed systematically. This reality is pushing sustainability management closer to the domains of data engineering, data integration, and enterprise information systems.

Ultimately, one of the most significant developments in the sustainability field is the transformation of sustainability data into a core informational layer generated within corporate systems. Sustainability reports are no longer merely communication tools; they are outputs of corporate data infrastructures. Consequently, sustainability management is becoming increasingly connected to data architecture, data governance, and enterprise information systems. In this context, competitive advantage in sustainability will increasingly depend on how robust and scalable a company’s underlying data infrastructure is.

8. Strategic Implications for Companies

The transformation taking place in the sustainability field affects not only reporting practices but also companies’ organizational structures, decision-making processes, and technology infrastructures. As sustainability data becomes increasingly integrated into the financial system and regulatory frameworks introduce more detailed disclosure requirements, sustainability management is evolving into a strategic corporate function. This development raises an important question for companies: should sustainability data be produced merely for reporting purposes, or should it become an integral component of corporate decision-making?

Under the traditional sustainability approach, sustainability data was often treated as an output of annual reporting processes. Indicators such as energy consumption, carbon emissions, or water usage were calculated at the end of a reporting period and disclosed in sustainability reports. However, the growing use of sustainability data in financial risk analysis and investment decision-making has demonstrated the limitations of this approach. If sustainability data is to support strategic decisions, it must be generated continuously and integrated with operational systems.

For this reason, many companies are beginning to approach sustainability management from a sustainability operations perspective. The sustainability operations approach treats sustainability data not only as a reporting output but also as an input for managing operational performance. Decisions related to energy efficiency investments, supply chain transformations, or improvements in production processes require the analysis of sustainability data. As a result, sustainability teams are increasingly connected to data analytics and operational management functions within organizations.

This transformation also enables the integration of sustainability data into decision support systems. One notable example is the emerging concept of carbon decision systems. Carbon decision systems refer to platforms that connect carbon emissions data with investment decisions, production planning, and supply chain strategies. These systems allow companies to analyze the carbon implications of different operational scenarios and evaluate lower-carbon alternatives. For instance, the selection of energy sources for a manufacturing facility or the optimization of logistics routes can directly influence carbon emissions. Supporting such decisions with sustainability data can significantly affect both environmental performance and long-term cost structures.

The integration of sustainability data into corporate decision-making also creates a new dimension of competitive advantage. In the past, sustainability performance was often evaluated primarily through communication strategies or corporate reputation management. However, as data infrastructures become more advanced, sustainability is increasingly linked to operational efficiency and strategic management. Reducing energy costs, managing supply chain risks, and developing low-carbon production processes all depend on the effective analysis of sustainability data.

Consequently, a strong sustainability data infrastructure can become a significant source of competitive advantage. Companies that can integrate sustainability data with operational systems and effectively analyze that data are better positioned to comply with regulatory requirements and to use sustainability performance as a strategic management tool. This shift transforms sustainability management from a purely compliance-driven activity into an integral component of corporate performance management.

This transformation is also reshaping the role of sustainability teams within organizations. Traditionally, sustainability teams often consisted of relatively small groups responsible primarily for managing reporting processes. However, as data infrastructures become more important, sustainability teams increasingly need to engage with data engineering, data analytics, and system integration. This development is closely connected to the emerging concept of ESG data governance.

ESG data governance aims to systematically manage how sustainability data is produced, which methodologies are used, and how the data is verified. This approach requires the integration of sustainability data into broader corporate data governance frameworks. Data quality controls, methodological management, and data traceability are becoming essential components of sustainability data governance.

This transformation has also led to the emergence of a new technology ecosystem in the sustainability field. Software platforms and data systems designed to support corporate sustainability infrastructures are becoming increasingly common. These platforms allow companies to collect sustainability data from operational systems, automate carbon calculations, and generate disclosures aligned with different reporting frameworks. Such systems help integrate sustainability data into the natural architecture of corporate information systems.

In this context, one concept that is increasingly discussed is that of sustainability operating systems. Sustainability operating systems refer to platforms that integrate the processes of collecting, calculating, and reporting sustainability data within a unified corporate system. These systems enable sustainability data to be used not only for reporting but also for strategic decision-making.

This transformation reveals an important reality about the future of sustainability. Sustainability performance is not determined solely by corporate targets or strategies; it is also shaped by the data infrastructures that measure and manage that performance. As a result, competitive advantage in sustainability management increasingly depends on the quality and robustness of these data infrastructures.

In recent years, a new generation of platforms has begun to develop infrastructures that integrate sustainability data directly with operational systems. Such platforms can help companies manage sustainability data more systematically and comply with evolving reporting standards. However, their true potential lies in enabling sustainability data to be used not only for reporting purposes but also for corporate decision-making.

Ultimately, the transformation occurring in the sustainability field does not simply represent the introduction of new reporting obligations for companies. It represents the integration of sustainability data into the core of corporate strategy. Companies that can integrate sustainability data with operational systems and incorporate it into strategic decision processes will gain a significant advantage in the coming years. The future of sustainability will depend not only on what goals companies set, but also on how those goals are measured and managed.

9. Conclusion — The Infrastructure Decade of Sustainability

At first glance, the developments that have taken place in corporate sustainability over the past two decades may appear to be primarily about the evolution of targets, strategies, and reporting standards. Companies have announced carbon neutrality commitments, published sustainability reports, and attempted to communicate their ESG performance to investors. Yet behind these developments, a deeper transformation has been unfolding. Sustainability is gradually moving beyond being a matter of narrative or corporate communication and is becoming a data infrastructure problem—one in which sustainability information is produced, processed, and managed within corporate systems.

As discussed throughout the previous sections of this article, this transformation is driven by several key dynamics. First, the growing economic materiality of sustainability issues within the financial system has led to the use of sustainability data in investment decision-making. Climate-related risks are no longer viewed solely as environmental concerns but also as financial risks. As a result, investors increasingly demand sustainability information that is reliable, comparable, and usable within financial decision processes.

Second, the increasing shift toward regulation-based sustainability reporting has significantly expanded the volume of data that companies are required to produce. Regulatory frameworks such as CSRD and ISSB are transforming sustainability reporting into complex disclosure regimes involving hundreds of data points. This development makes it increasingly difficult to manage sustainability data through manual processes alone.

Third, the nature of sustainability data production—being deeply dependent on operational systems—has transformed sustainability management into a technical data architecture challenge. Sustainability metrics rely on multiple operational data sources, including energy consumption, production activities, logistics movements, and supply chain operations. Integrating, calculating, and reporting these datasets requires robust corporate data infrastructures.

Taken together, these developments indicate that the sustainability field is entering a new phase. In this new phase, sustainability performance will no longer be determined solely by the quality of corporate targets or strategies. The decisive factor will increasingly be how sustainability data is produced and governed. In other words, competition in sustainability is gradually shifting toward the strength of underlying data infrastructures.

From this perspective, the coming decade can be described as the infrastructure decade of sustainability. Companies will need to develop data architectures capable of integrating sustainability data with operational systems, managing calculation methodologies transparently, and producing disclosures aligned with multiple reporting standards. These infrastructures will be essential not only for regulatory compliance but also for using sustainability data within strategic decision-making processes.

In this context, a clear distinction is beginning to emerge among companies. On one side are organizations that still view sustainability primarily as a reporting exercise. In this model, sustainability performance is treated largely as the output of reports published at the end of the year. On the other side are companies that design sustainability as a component of their corporate data infrastructure. These companies develop systems capable of generating sustainability data directly from operational processes, analyzing that data, and integrating it into strategic decision-making.

As a result, the central question in corporate sustainability is becoming increasingly fundamental:

Can companies truly manage sustainability data, or can they only report it?

The answer to this question will determine which organizations will be able to achieve genuine transformation in the years ahead. The future of sustainability will not depend solely on the targets companies set, but on the data infrastructures that support how those targets are measured and managed.

References

Berg, F., Kölbel, J. F., & Rigobon, R. (2019).

Aggregate Confusion: The Divergence of ESG Ratings.

MIT Sloan School of Management Working Paper.Clark, G. L., Feiner, A., & Viehs, M. (2015).

From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance.

University of Oxford & Arabesque Partners.Financial Stability Board. (2017–2023).

Task Force on Climate-related Financial Disclosures (TCFD) Reports and Status Reports.

Financial Stability Board.European Commission. (2022).

Corporate Sustainability Reporting Directive (CSRD).

European Commission.Greenhouse Gas Protocol. (2011).

Corporate Value Chain (Scope 3) Accounting and Reporting Standard.

World Resources Institute & World Business Council for Sustainable Development.International Energy Agency. (IEA). (2023).

Emission Factors and Energy System Data Methodologies.

International Energy Agency.Ioannou, I., & Serafeim, G. (2011).

The Consequences of Mandatory Corporate Sustainability Reporting.

Harvard Business School Working Paper No. 11-100.IFRS Foundation. (2023).

International Sustainability Standards Board (ISSB) – General Requirements for Disclosure of Sustainability-related Financial Information.

IFRS Foundation.Oxford University / Smith School of Enterprise and the Environment. (2015).

From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance.United Nations Principles for Responsible Investment (PRI). (2020).

Principles for Responsible Investment.